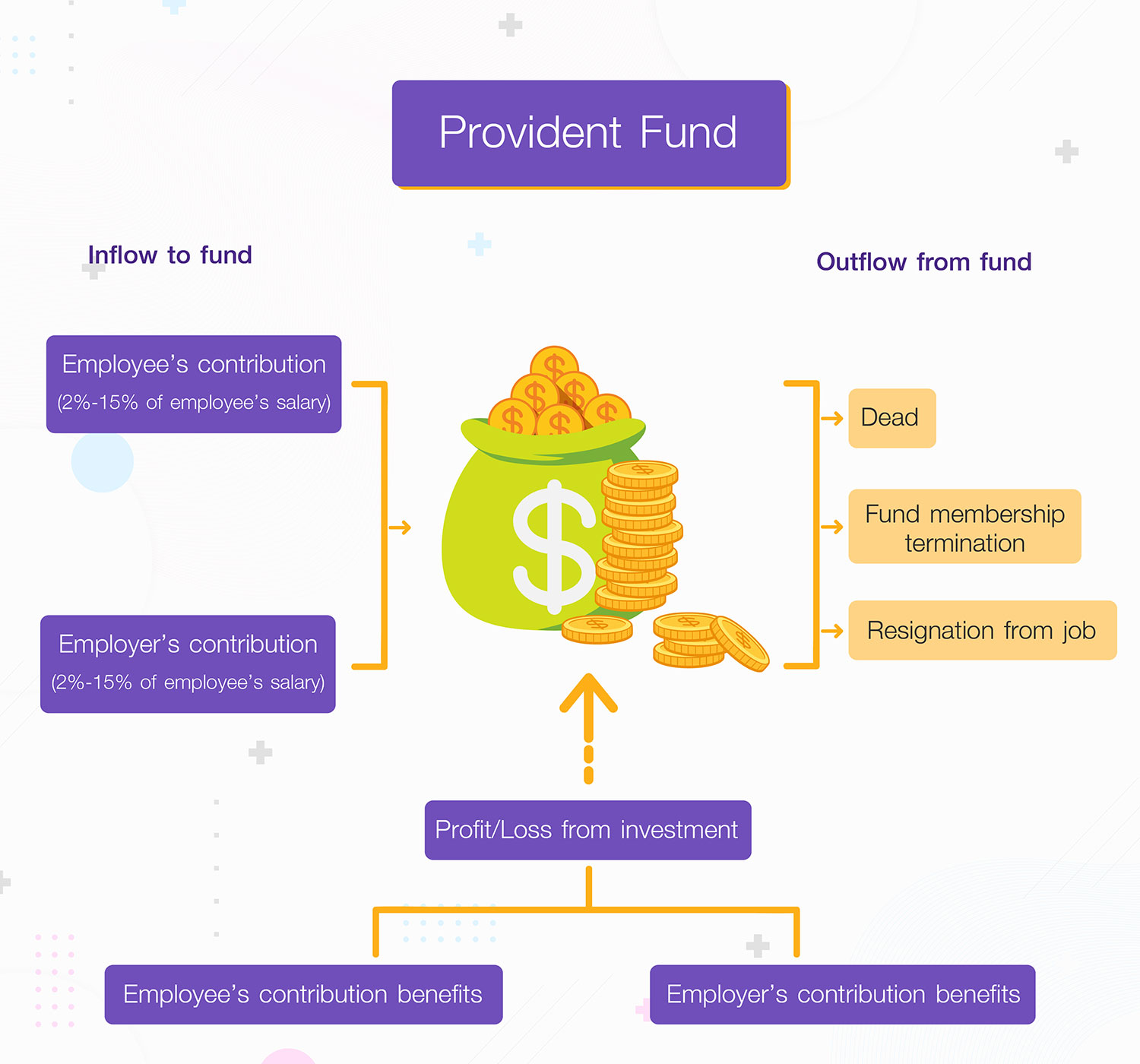

A provident fund is an investment fund that is voluntarily established by Employer and employees to serve as long term savings to support an employee’s retirement.

Sources of fund:

Fund placed in a provident fund will be managed by an investment management company in accordance with a specified investment policy to maximize the financial returns, given the acceptable risk level.

The provident fund, registered with the Securities and Exchange Commission (SEC), is a unique legal entity which is fully separated from the employer and the investment management company. Employees (provident fund members) can therefore be confident that if the employer or the investment management company becomes financially insolvent, the fund’s assets will not be affected by any liabilities the employer or the investment management company may have.

Provident fund components

1) Investment management

• Strengthens the employer’s image as a solid company that values staff welfare

• Increases employee’s confidence in the business, thereby enhancing staff performance

• Builds a strong relationship between the employer and employees, minimizing potential for labour disputes

• Decreases employee turnover and increases staff loyalty for longer service with the company

2) Financial security

• Encourages planning for long-term savings

• Financial security for the member and family upon retirement, resignation, or death.

3) Return on investment

• Additional benefit from the employer’s contribution made each month

• Earn returns from the provident fund in the form of interest, dividends or capital gains. Members can potentially

earn a higher return than placing the sum in a bank deposit. The level of returns is dependent on the fund

scheme selected or the risk tolerance level specified by the member. The investment will be professionally managed

by a qualified and experienced investment management company.

• Savings through the provident fund is a continuous process, despite resigning and switching to work for

another employer. The investment can be kept with the original fund (maintain) or transferred into another

provident fund.

• Upon retirement, the member may also keep the balance in the fund (maintain) or may choose to withdraw

the sum as annuities, in order to continue generating returns on the investment.

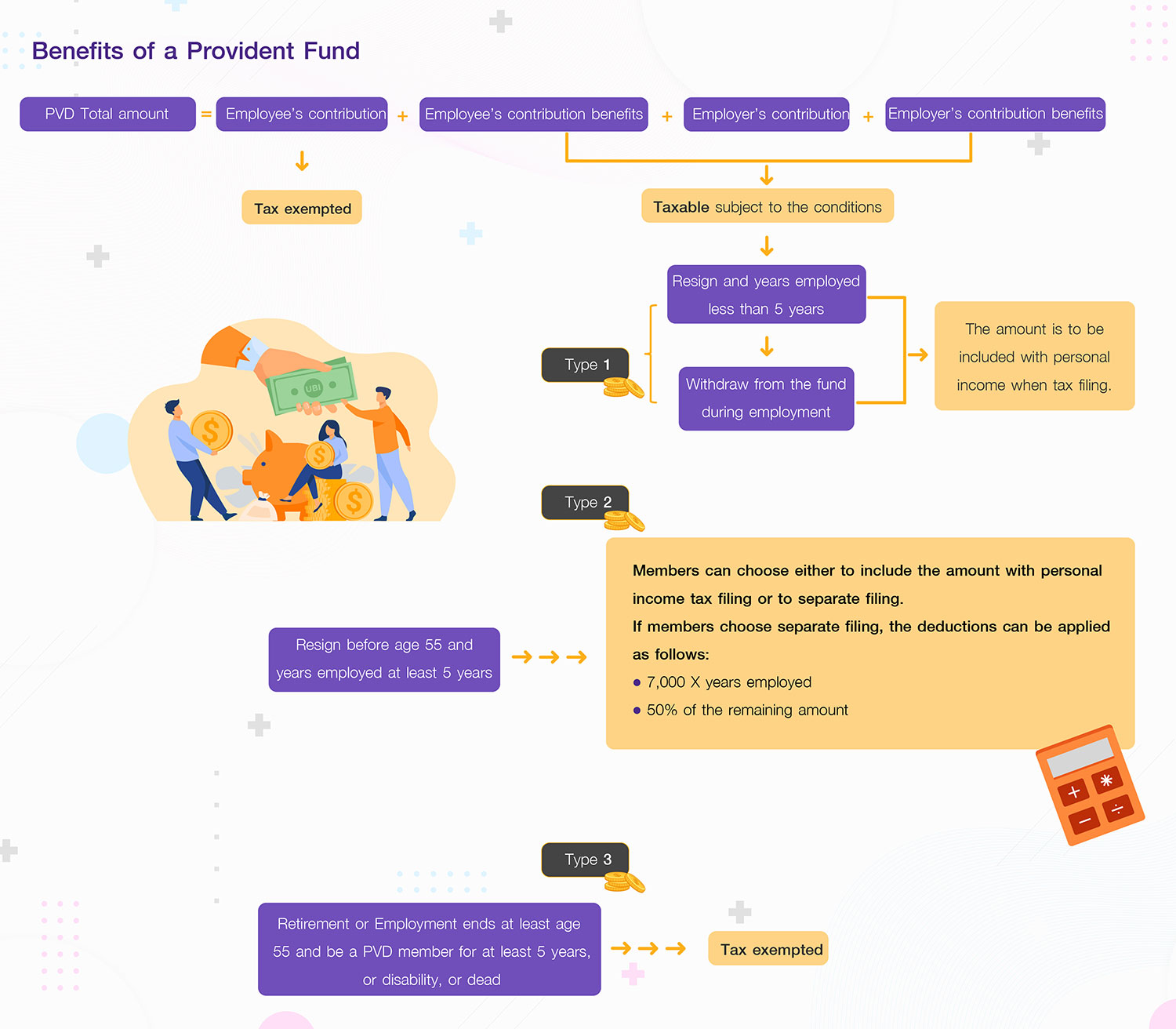

4) Tax

• The employer receives a tax allowance on the employer contribution by deducting it as an expense of the

company when determining net income subjected to taxes. Actual amount can be deducted, but not

exceeding 15% of each employee’s salary.

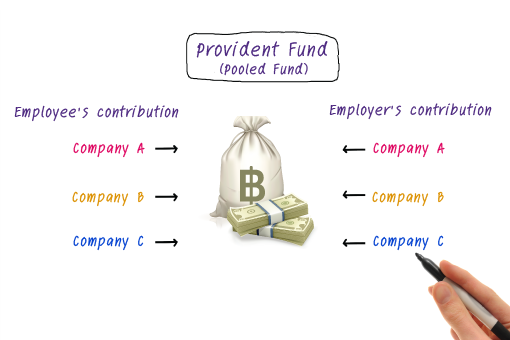

1. Single Fund refers to a provident fund established by only one employer

2. Pooled Fund refers to a fund which is jointly established by 2 or more employers. The employers can either be affiliated companies in the same group or unrelated.

Remarks:

The investment policy governs how the providend fund is managed and is jointly agreed between the Provident Fund Committee and the investment management company. Typically, the investment policy will specify the asset class and portfolio weightings of each type of investible asset that the fund allows the investment manager to invest in. The investment policy should be configured to match the objectives and risk tolerance of members.

However, having only one uniform investment policy may not be an ideal way of catering to each employee’s different requirements. As such, a means was pursued to enable each employee to be able to choose an investment policy to suit oneself and this had led to the introduction of the Employee’s Choice feature.

Employee’s Choice is a scheme whereby the employee is able to influence the choice of investment policy that is suited to one’s needs. SCBAM wishes to therefore propose the Employee’s Choice feature based on various investment policies. This allows each member of the provident fund the ability to select the investment policy that one considers most appropriate to one’s needs and acceptable risk level. This is illustrated in the diagram below.

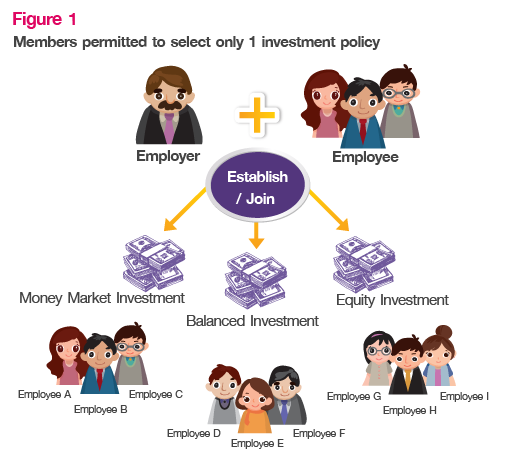

1. Choice to select an investment policy

Although there are many available choices, a member may only choose one investment policy and the proceeds are all invested according to the chosen investment policy that each particular member has selected.

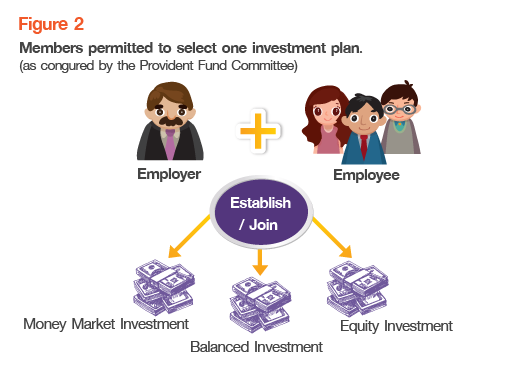

2. Choice to select an investment plan

The employer may offer several investment plans to choose from, whereby each investment plan consist of different portfolio weightings as prescribed. A member is permitted to choose one investment plan that is suitable with a risk level that

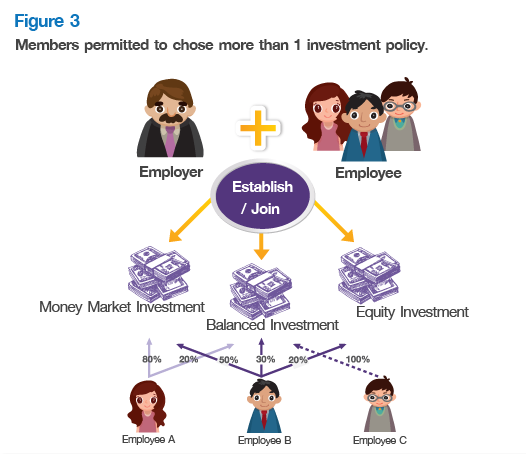

3. Choice of selecting your own investment weightings (DIY)

Under this feature, the employer offers several investment policies to choose from and allows members to select the investment policies and portfolio weightings as desired in order to help achieve good diversification. The employer’s contribution and the employee’s contribution shall be allocated in accordance to the portfolio allocation selected. The return on the investment will be dependent on the returns generated by each of the investment policies.